Your Dispute Strategy in Action

By now, sellers realize that the consumer trend away from in-store shopping and toward e-commerce is not going to reverse any time soon. In fact, a recent study reported that 44% of global consumers now purchase physical goods online.1

With so much new online purchasing and so many businesses moving online, are CNP sellers developing the right dispute strategies to manage this new payments landscape? Are they deploying the right technology? Do they have the right processes in place? And are they testing to make sure their dispute strategy is effective? Knowing the answers to these questions is essential for any CNP business that wants to minimize the impact of disputes.

Analyze Your Dispute Threat and Secure Your Defenses

Whatever tactics you may have currently implemented to reduce the risk of disputes, it’s best to begin by examining them and their effectiveness. While you may have best-known tools to prevent and reduce the risk of fraud, no matter what efforts you make in the early part of the transaction life cycle, first-party fraud or friendly fraud can be seen as a path that some bad actors take to game the system. When a customer commits first-party fraud or friendly fraud, they are disputing a valid transaction they don’t recognize – or claim not to. In both cases, the purchases are legitimate. The difference with the latter case is that these customers are intentionally challenging legitimate purchases as fraudulent to regain funds. In fact, in a recent survey report, 16% of consumers who were contacted admitted to perpetrating friendly fraud2 – adding a cautionary note that this number is likely conservative. This statistic sends a clear message that sellers need to apply dispute management tactics in the post-purchase environment to reduce friendly fraud and the resulting disputes.

Whatever tactics you may have currently implemented to reduce the risk of disputes, it’s best to begin by examining them and their effectiveness. While you may have best-known tools to prevent and reduce the risk of fraud, no matter what efforts you make in the early part of the transaction life cycle, first-party fraud or friendly fraud can be seen as a path that some bad actors take to game the system. When a customer commits first-party fraud or friendly fraud, they are disputing a valid transaction they don’t recognize – or claim not to. In both cases, the purchases are legitimate. The difference with the latter case is that these customers are intentionally challenging legitimate purchases as fraudulent to regain funds. In fact, in a recent survey report, 16% of consumers who were contacted admitted to perpetrating friendly fraud2 – adding a cautionary note that this number is likely conservative. This statistic sends a clear message that sellers need to apply dispute management tactics in the post-purchase environment to reduce friendly fraud and the resulting disputes.

Start by looking for gaps in your payment processes with vulnerabilities to fraud and disputes. Are you using authentication tools to stop fraud and defer liability? Are you identifying disputes stemming from dissatisfaction with products or services? Are you collecting the best evidence for dispute responses and revenue recovery? Find the holes and fill them before stress-testing your strategy.

Every dispute management strategy is unique, and each seller has specific needs and goals.

Consider the following tactics to help test and strengthen your dispute strategy to better protect your business throughout the payments life cycle:

Pre-Authorization

At the pre-authorization stage, the seller’s objective is to find the right balance between fraud prevention and authorizations to meet revenue targets. Different categories of sellers will have different business needs, so it’s important for each seller to determine the mix of fraud prevention and authorizations that works best for their business and test against it. As an example, high-risk sellers with subscription-based businesses or that deal in intangible goods may experience larger dispute volume. These businesses may consider decreasing their fraud prevention measures to allow more authorizations, thereby spreading the cost of disputes over a larger revenue figure.

Post-Transaction

After the customer has made their purchase, sellers can sometimes feel powerless to prevent a dispute, should the customer choose to file one. Fortunately, there are actions sellers can take and solutions to reduce risk provided by the right partner. The first tactic is post-purchase outreach and communication. Follow up any transaction with a confirmation email, tracking information, and/or delivery status. To ensure your communications are effective, check email open rates, click-through rates, and A/B test subject lines. Additionally, collaborate with your customer service to capture their findings on customer responses and success metrics.

After the customer has made their purchase, sellers can sometimes feel powerless to prevent a dispute, should the customer choose to file one. Fortunately, there are actions sellers can take and solutions to reduce risk provided by the right partner. The first tactic is post-purchase outreach and communication. Follow up any transaction with a confirmation email, tracking information, and/or delivery status. To ensure your communications are effective, check email open rates, click-through rates, and A/B test subject lines. Additionally, collaborate with your customer service to capture their findings on customer responses and success metrics.

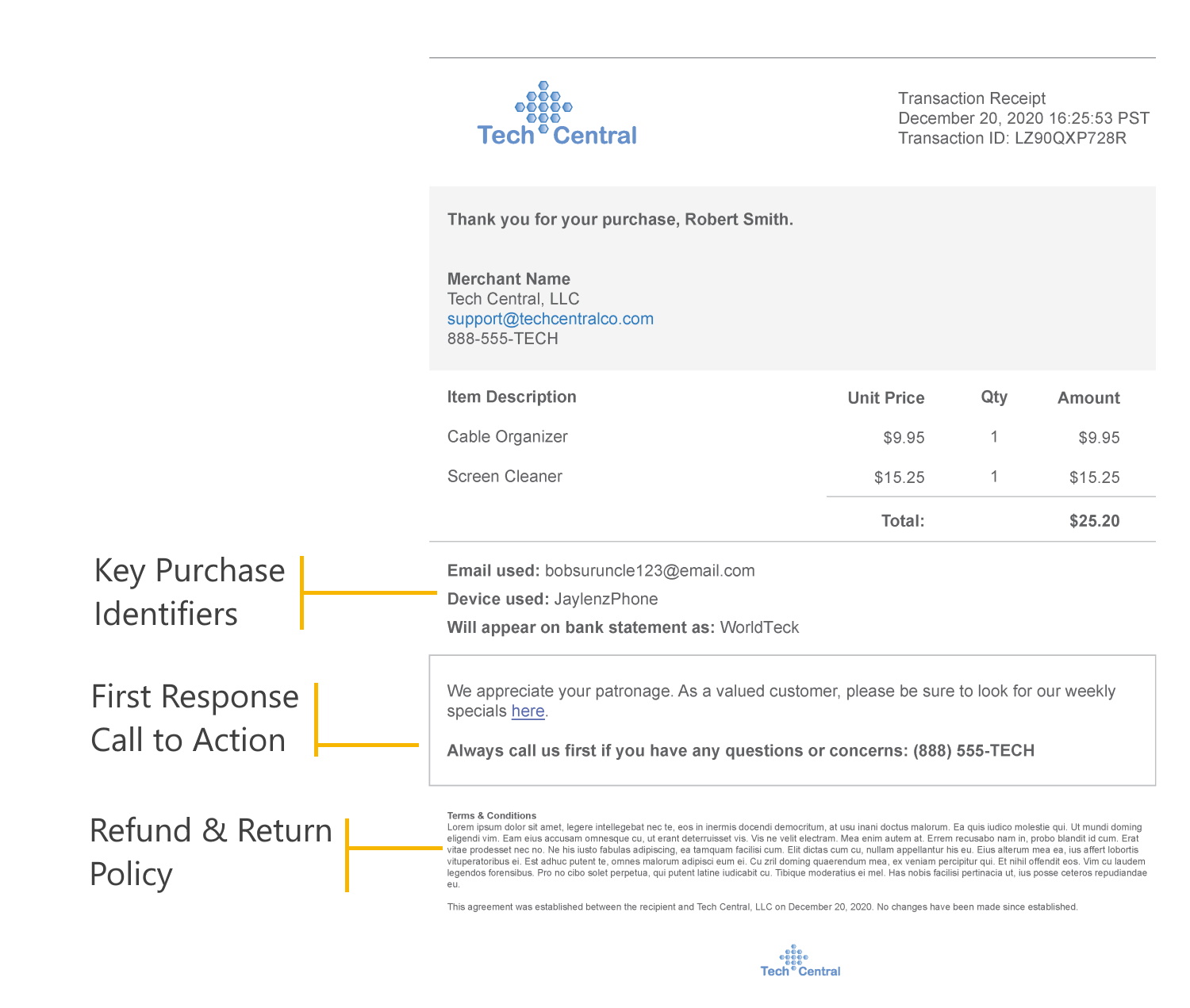

As a best practice, sellers should be proactive about communicating service policies for returns/refunds and T&C to customers by including these policies in post-transaction communications or even during checkout as a condition for completing an order. However you choose to surface your policies, they should also be clearly displayed on your website and easy to find. Measuring the amount of traffic leading to your policy pages can indicate the potential for their visibility to your customers. If traffic to policy pages is low compared to the amount of customer service interaction on issues involving service policies, then sellers may need to increase visibility on their policy web pages to help reduce operational strain.

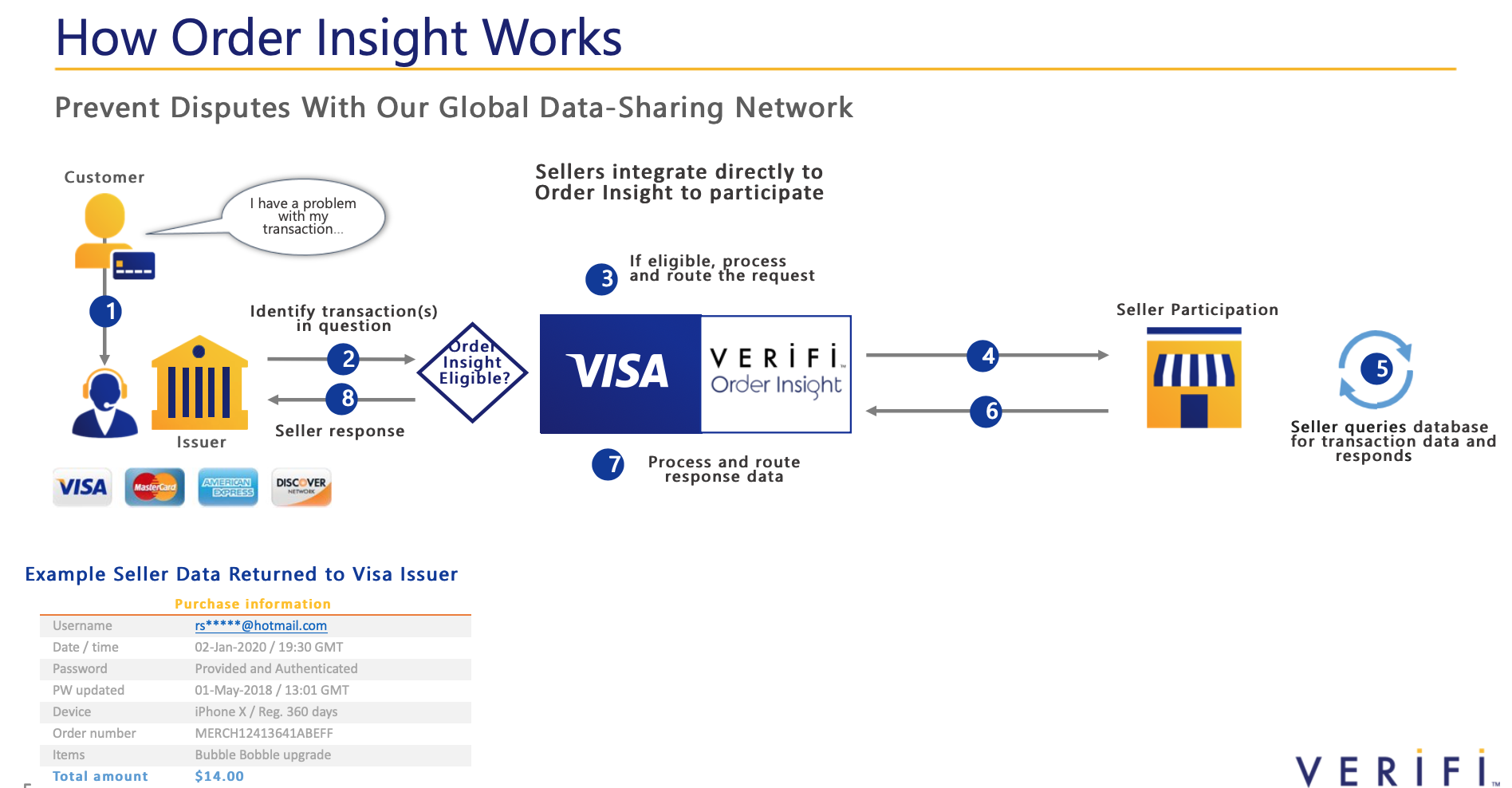

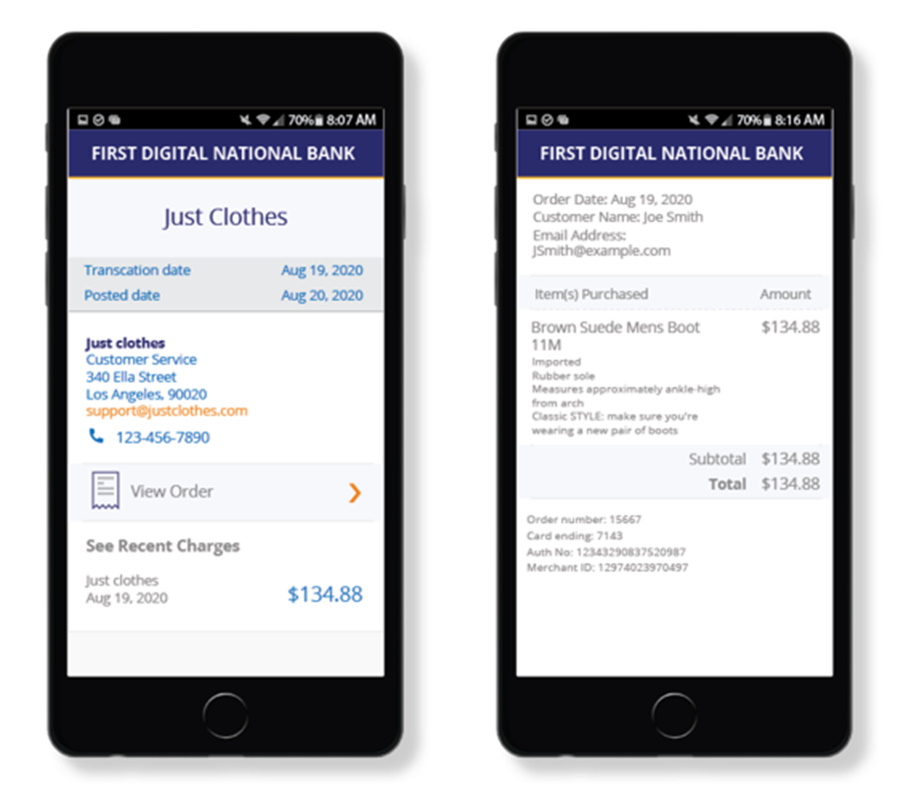

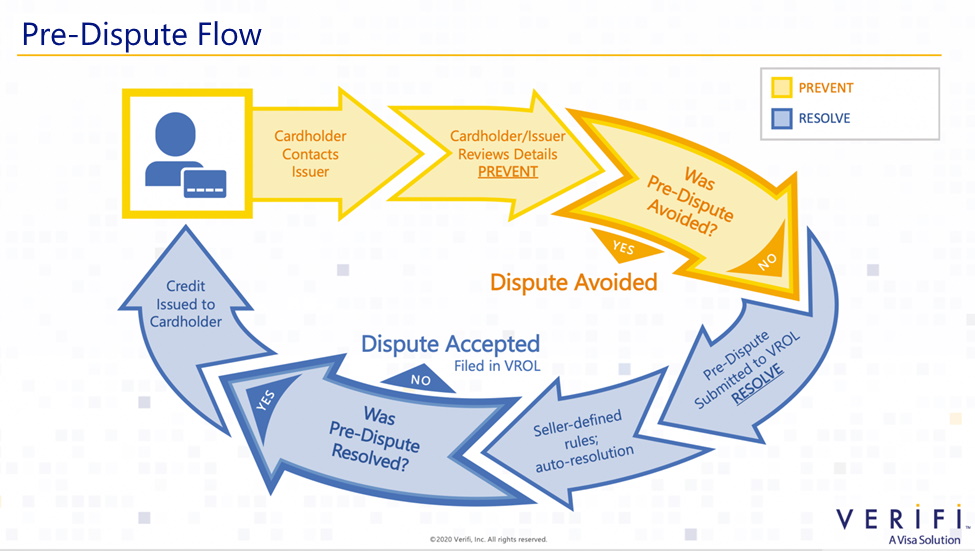

The goal is to convince your customer to work with you instead of their bank if there’s an issue with the customer’s transaction. When the customer does contact you, ensure to have processes in place to offer a refund or credit voucher to save the relationship. Another tactic is to take advantage of seller-issuer collaboration technologies. These solutions can enable sellers to engage with quick responses to prevent the dispute, provide a resolution, or accept liability to potentially fight the dispute later. Such collaboration solutions involve a level of automation to help identify transaction information to prevent a dispute at inquiry, as well as provide a quick resolution by refund, if warranted, stopping a chargeback from ever occurring.

Dispute Response & Recovery

When it comes to chargebacks, sellers are simply leaving money on the table. Chargebacks don’t have to be accepted as just part of doing business. If you know that you’ve made a valid sale, then it’s worth the effort to recover revenue that you’ve rightfully earned. With the right resources and know-how, an in-house dispute management team can build effective dispute responses to recover funds. Third-party services, however, can do the heavy lifting for you, employing expert tactics to aggregate dispute source data, assemble the best-case evidence, and prepare and deliver dispute responses in the proper time frame.

To decide whether to represent in-house or outsource, sellers must measure operational cost against the cost of a third-party service. Sellers must calculate human capital, benefits, and overhead operational costs – not just payroll – before making a decision.

Sellers should also consider their overall representment rate. For example, what is the percentage of chargebacks that are being represented out of the total number of chargebacks received? By reviewing the total number of chargebacks, there may be opportunities to increase revenue recovery by representing more cases. In addition, consider the net win rate of your chargebacks vs. your gross win rate. After all, customers can resubmit a dispute even after successful revenue recovery.

Whether your dispute management is performed in house or by a partner, these tips can help maximize your recovery wins:

- A/B test response packages with multiple acquirers for insights on which formats work best for response wins.

- Use reports from dispute case management tracking to understand fraud and reason codes that might cause most common dispute cases, then update operations to prevent them.

- From your CRM and dispute source data, identify customers who are disputing transactions and why. If necessary, block from future transactions.

Refine Your Dispute Strategy, Test Again

Your dispute strategy will never be finished. As long as the payments landscape keeps shifting, your dispute strategy must be ready to accommodate those changes. That means constant review of your tactics. Are your security measures creating too much friction and causing missed sales opportunities? Are your measures too lax and allowing too much fraud through? How many representments are you acting on, and can you do more? Are there seasonal spikes in your chargebacks? Answers to these questions and more will inform how you adjust for the best possible dispute strategy that works for you and your customers.

Your dispute strategy will never be finished. As long as the payments landscape keeps shifting, your dispute strategy must be ready to accommodate those changes. That means constant review of your tactics. Are your security measures creating too much friction and causing missed sales opportunities? Are your measures too lax and allowing too much fraud through? How many representments are you acting on, and can you do more? Are there seasonal spikes in your chargebacks? Answers to these questions and more will inform how you adjust for the best possible dispute strategy that works for you and your customers.

This clear-eyed analysis of your technology and processes in all stages of the transaction life cycle can help reduce fraud and disputes, improve your customers’ experience, and set your business up for continued success and growth.

Want more? Don’t forget to read our previous blog post “Top 3 Ways to Improve Your Dispute Strategy”.

1 Mobile & Online Remote Payments for Digital & Physical Goods – Juniper Research, 2019-2024

2 Improving the Dispute Experience: Transparency Is Power – Aité, 2020

While chargebacks do cause losses in revenue, for some sellers, time may be the greatest cost when managing disputes and chargebacks. If that’s the case, then the expense is made at otherwise growing their customer base and loyalty.

While chargebacks do cause losses in revenue, for some sellers, time may be the greatest cost when managing disputes and chargebacks. If that’s the case, then the expense is made at otherwise growing their customer base and loyalty.